How Indians Are Actually Managing Money in 2026 | SIP, UPI & Wealth Trends

Personal Finance · India 2026 · April 23, 2026 · 8 min read · Data-backed analysis

---

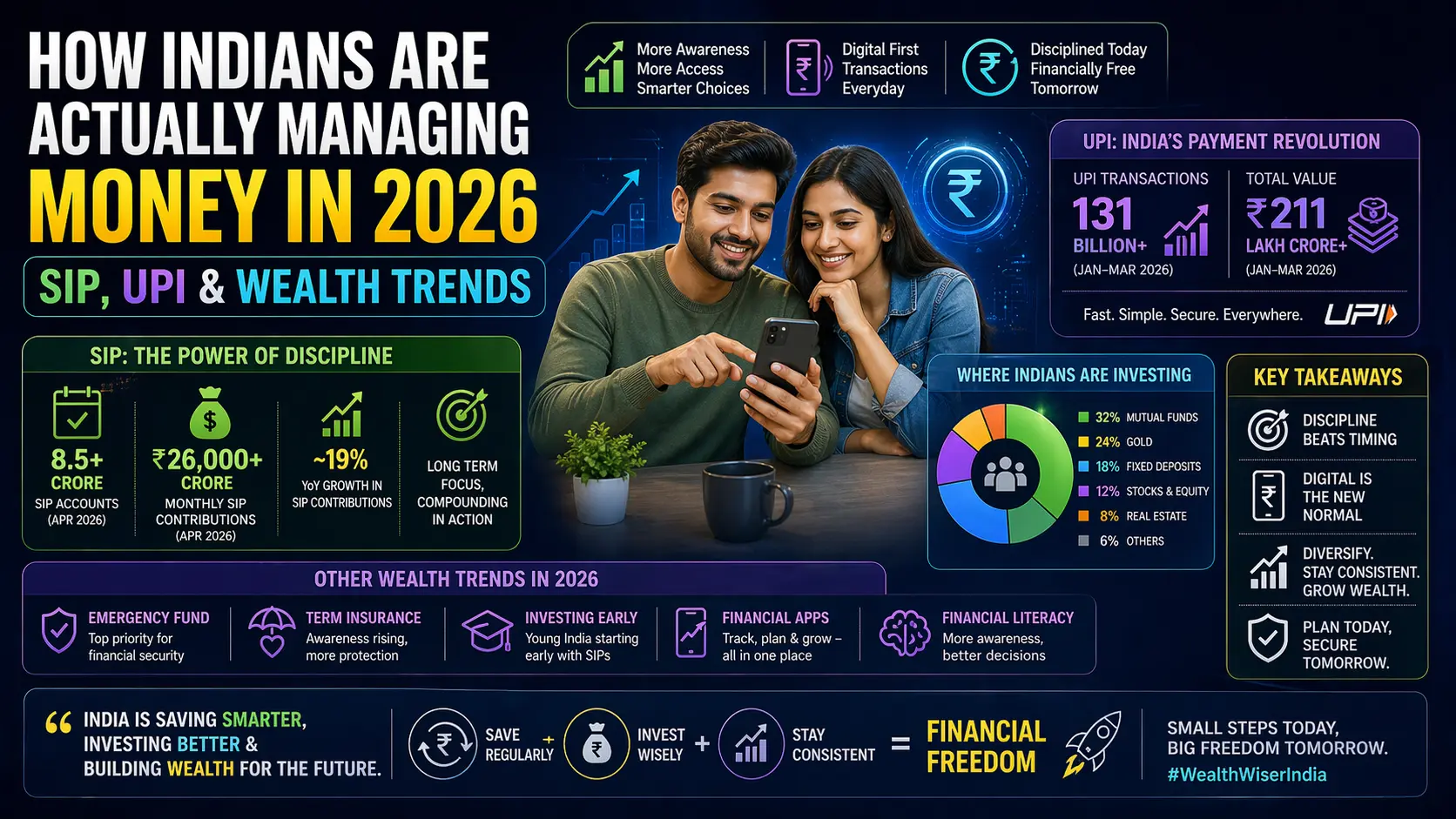

> Key Stats at a Glance

> - 💰 ₹81 Lakh Crore — Mutual Fund AUM

> - 📱 500M+ — UPI Unique Users

> - 📈 9.44 Crore — Active SIP Accounts

> - 🔁 21.63 Billion — UPI Transactions (Dec 2025)

> - 🏦 215 Million — Demat Accounts

---

There's a version of this article that calls all of this a "financial revolution" and sprinkles phrases like "democratising wealth" every other paragraph. This isn't that version. What's actually happening in India's personal finance landscape in 2026 is more interesting — and more complicated — than those phrases suggest.

---

📊 The SIP Story Is Real — and It's Not Stopping

Monthly SIP inflows in India have been above ₹29,000 crore every single month in early 2026. January hit ₹31,002 crore. February came in at ₹29,845 crore — slightly lower, but still 14.8% higher than February 2025. The mutual fund industry's total AUM is now above ₹81 lakh crore, up from ₹22 lakh crore just five years ago.

Here's the part people miss: this is not investor euphoria. Markets have been volatile in early 2026. FPIs pulled money out. Indices have wobbled. And yet SIP contributions kept flowing in — because most retail investors doing SIPs have essentially automated their behaviour out of their own emotional control. That's actually the point of the product.

> "Staying invested is more important than predicting tops and bottoms."

> It's boring advice. It's also the one that's proven right again and again.

SIP by the Numbers

| Metric | Figure | Context |

|--------|--------|---------|

| SIP inflows — January 2026 | ₹31,002 Cr | Record high monthly contribution |

| Active SIP accounts | 9.44 Crore | Up from 8.26 crore a year ago |

| SIP share of total MF AUM | 20.3% | ~₹16.64 lakh crore in SIP assets |

The shift is also geographic. Two years ago, SIP growth was largely a Tier-1 city story. Now Tier-2 and Tier-3 cities are contributing meaningfully to new folios. Simpler digital onboarding, improved financial literacy, and apps that work in regional languages have done more for retail investing than any government campaign.

> 🟢 For New Investors

> If you haven't started a SIP yet, the case for doing it is stronger in 2026 than it was five years ago — not because markets are in a bull run, but because the infrastructure around it (lower costs, fractional investing, instant KYC) is genuinely better. Starting with ₹500 a month is a real option now.

---

👤 Under-30s Are Actually Investing — Not Just Trading

The stereotype of young investors in India has been F&O speculation — high-leverage derivatives trading that bleeds money. That stereotype isn't wrong, but it's incomplete.

As of February 2026, investors under 30 make up 38.4% of active equity market participants, up from 22.6% in March 2019. That's a huge demographic shift in six years. And more importantly, the SIP data suggests a meaningful chunk of this cohort is doing boring, sensible things — setting up monthly SIPs, picking diversified equity funds, and not touching them.

This matters for the long-term picture. A 26-year-old starting a SIP today has 35 years of compounding ahead. India's mutual fund industry is still, structurally, in the early stages of capturing household savings. Equity participation sits below 10% of Indian adults, compared to around 55–60% in the US. The runway is long.

> 🟡 One Thing to Watch

> Of 12.8 crore registered investors, only 1.48 crore were active as of February 2026. That gap between registered and active accounts is worth paying attention to — a lot of people have demat accounts they opened during 2020-21 and haven't touched since. Not all of this cohort will stay engaged.

---

📱 UPI Has Won. The Next Fight Is What Gets Built on Top of It.

In December 2025, UPI processed 21.63 billion transactions — the highest ever, and roughly 50% of all real-time digital payment volume globally. That number is almost too large to mean anything on its own, so here's a frame that helps: India's annual UPI transaction value in 2025 was approximately $3.4 trillion. Global e-commerce in 2024 was around $6 trillion. UPI's value is already more than half that.

The payments battle in India is essentially over. PhonePe and Google Pay dominate volume. The interesting competition has shifted to what sits on top of payments: lending, insurance, wealth products, credit lines. PhonePe's financial services revenue — insurance and lending — grew 206% in FY2025. That's where the money is, because UPI's zero-MDR policy means nobody actually earns on the payments themselves.

UPI: A Quick Timeline

| Year | Milestone |

|------|-----------|

| Early 2026 | UPI crosses 500M unique users. RuPay credit cards seeing widespread merchant acceptance. |

| 2025 | 228.3 billion transactions worth $3.4 trillion. AutoPay mandates hit 1.27 billion in November alone. |

| 2024–25 | Cross-border UPI transactions grew 1,936% year-over-year. Active in Singapore, UAE, France, Bhutan, Sri Lanka. |

| Now | High-value limit raised to ₹10 lakh for insurance & capital markets. Projected 1 billion transactions/day by FY2028. |

UPI Lite — the offline, low-connectivity version — now supports transactions up to ₹5,000 and has expanded meaningfully into semi-urban and rural markets. This is where actual financial inclusion lives: not in the cities that already have bank branches, but in places that don't.

---

🏦 215 Million Demat Accounts — But Active Investors Are a Different Story

Demat accounts in India grew from 39.4 million in 2019 to 215.9 million by December 2025. That's a 5.5x increase in six years. It happened because opening an account went from a week-long paperwork exercise to a 10-minute Aadhaar-verified mobile process. Remove friction, get volume.

But account count is the easy metric. The harder question is what people actually do with them. Of all registered investors, only about 1.48 crore were genuinely active as of early 2026 — meaning roughly 90% of demat accounts sit dormant or semi-dormant. This isn't surprising for any platform with frictionless onboarding, but it does mean the "democratisation of investing" narrative needs a footnote.

What is genuinely encouraging: Domestic Institutional Investors (DIIs) — driven in large part by mutual fund inflows — now hold a record 17.82% stake in NSE-listed companies. That makes the market structurally less dependent on FPI flows than it was five years ago. When foreign investors pulled $52 billion from Asian markets in early 2026, India's indices wobbled but didn't collapse. Domestic capital cushioned the fall.

---

💳 BNPL and Digital Credit: Growing Fast, Needs Watching

India's buy-now-pay-later market reached $24.86 billion in 2025 and is projected to hit $30.45 billion in 2026. UPI-linked BNPL grew at 34.2% CAGR from 2022 to 2025. The access story is real — fintech lenders now hold 47% of the unsecured personal loan market and 73% of loans below ₹1 lakh, reaching segments that banks historically ignored.

The other side of this is default rates. Lenders like KreditBee, Nira, and Dhani operate in high-risk, short-tenure lending, and their default figures are steep. After years of rapid expansion, 2026 is starting to look like a year of discipline — better underwriting, co-lending models with banks, and the RBI keeping a close eye on the sector.

> 🔵 A Practical Note

> BNPL and easy EMI options on UPI are genuinely useful for large purchases. They're expensive money when used for daily consumption. If you find yourself rolling over BNPL balances month-to-month, the effective interest rate is typically between 24–36% annualised. That math gets ugly fast.

---

🎯 What This Actually Means If You're an Individual Investor

If you step back from all the numbers, a few things stand out for anyone trying to navigate their own finances in 2026.

SIPs have become the default savings vehicle for salaried Indians in a way that fixed deposits were for the previous generation. The shift isn't complete, but it's happening. If your emergency fund is sorted and you're not investing yet, the case for starting is real.

Digital payments have simplified daily transactions to the point where managing cash flow is easier than it's ever been. That's genuinely useful. The flip side is that it's also easier to spend — UPI and BNPL both reduce friction in the direction of outflows, not just inflows.

The wealth management side is expanding too. Platforms are now offering portfolio analytics, goal-based planning, and access to alternative investments — things that used to require a private bank relationship or a minimum Rs. 50 lakh investable corpus. That barrier is dropping. It's worth exploring what's available, even if you're early in your wealth-building journey.

One caveat: the fintech landscape is changing fast enough that regulatory risk is real. The Paytm Payments Bank episode in 2024 was a reminder that even large, widely used platforms can hit existential problems with the regulator. Stick with platforms backed by regulated entities and don't keep significant money in wallets you'd panic about losing access to.

---

> Disclaimer: This article is for informational and educational purposes only. It is not investment advice. All investments carry risk. Consult a SEBI-registered investment adviser before making financial decisions.

---

Sources: AMFI, ICRA Analytics, Digital in Asia, NPCI, SEBI, CoinLaw, PRS India, AngelOne, HDFC Sky.